Imagine walking out of your doctor's office with a prescription for a life-changing medication, only to find out at the pharmacy counter that it costs more than your monthly rent. It’s a nightmare scenario that plays out for millions of people every year. According to recent research by GoodRx, about 22% of patients abandon their prescriptions simply because they can’t afford them. That is one in five people leaving without the medicine they need.

The good news? You don't have to wait until you reach the pharmacy to find out what you're paying. In fact, discussing prescription cost and coverage before you even leave the provider's office is now considered a standard part of patient-centered care. With new federal laws like the Inflation Reduction Act changing how much we pay for drugs in 2025 and 2026, knowing your rights and tools can save you hundreds-or even thousands-of dollars.

Why Talking About Money Matters More Than Ever

We often feel awkward bringing up money when talking to our doctors. We worry it might seem rude or that it will distract from our health concerns. But here is the reality: financial stress directly impacts your physical health. If you can't afford your meds, you skip doses. A study published in the *Journal of General Internal Medicine* found that patients who discuss costs with their providers are 37% less likely to skip doses due to cost.

Since 2018, the American Medical Association (AMA) has formally recommended that doctors talk about costs during clinical encounters. Why? Because a treatment plan that you can't afford is not a treatment plan-it's just a piece of paper. Dr. Kao-Ping Chua, a researcher at the University of Michigan, noted that while 30% of patients experience cost-related nonadherence, only 15% actually report routinely discussing these costs with their providers. That gap is where we need to focus.

By initiating this conversation, you empower your healthcare team to work with you, not against you. They can switch brands, adjust dosages, or apply for assistance programs before the bill hits your inbox.

Understanding Your Insurance Tiers and Deductibles

To have an informed discussion, you first need to understand the language your insurance company uses. Most commercial plans use a "formulary," which is a list of covered drugs divided into tiers. Think of tiers like shelves in a grocery store-the lower the shelf, the cheaper the item.

- Tier 1 (Generics): Usually the cheapest option, often requiring a small copay of $5 to $15.

- Tier 2 (Preferred Brand Name): Moderate cost, typically ranging from $25 to $50 per fill.

- Tier 3 (Non-Preferred Brand Name): Higher cost, often between $50 and $100.

- Specialty Tier: For complex conditions. These can be incredibly expensive, sometimes costing 25-33% coinsurance with no upper limit in many commercial plans.

Then there is the deductible. This is the amount you must pay out-of-pocket before your insurance starts covering its share. If you have a high-deductible health plan (HDHP), you might be on the hook for the full price of your medication until you've spent several hundred dollars early in the year. According to KFF analysis, individual marketplace plans averaged a $480 deductible in 2023. If your doctor prescribes a Tier 3 drug in January, you could be paying full price. Asking, "Am I past my deductible yet?" is a crucial question.

Key Questions to Ask Your Doctor

You don't need to be an insurance expert to navigate this. You just need to ask the right questions. The Pharmaceutical Research and Manufacturers of America (PhRMA) suggests five essential questions, but let's simplify them for your next appointment.

- "Is there a generic version of this medication?" Generics contain the same active ingredients as brand-name drugs but cost significantly less. If your doctor prescribes a brand name, ask if a generic exists.

- "Are there therapeutic alternatives that are covered by my insurance?" Sometimes, a different drug in the same class works just as well but sits on a lower tier of your formulary.

- "What is the estimated out-of-pocket cost for me specifically?" Don't accept vague answers. Ask for a number. If they don't know, ask them to check using their electronic health record tools.

- "Do I need prior authorization?" Some drugs require your doctor to get special permission from your insurer before they cover it. This process can take days or weeks. Knowing this upfront prevents delays.

- "Are there manufacturer coupons or patient assistance programs available?" Many pharmaceutical companies offer savings cards or free drug programs for eligible patients.

Dr. Aaron Kesselheim from Harvard Medical School pointed out that formulary complexity creates barriers, with 63% of physicians reporting difficulty determining patient-specific costs. By asking these questions, you help bridge that gap.

Tools to Check Costs Before You Go to the Pharmacy

You aren't limited to just asking your doctor. There are powerful digital tools designed to give you transparency.

GoodRx is a widely used platform that compares prescription prices across pharmacies and offers discount coupons. It holds about 70% of the market share for prescription savings tools. Users frequently report saving hundreds of dollars by showing their pharmacist a GoodRx coupon alongside their insurance card. However, remember that if you use a GoodRx coupon, those payments usually do not count toward your insurance deductible.

If you have commercial insurance, look for tools like CVS Caremark's "Check Drug Cost & Coverage." Available since 2019, it lets you input medication details to see immediate coverage status and copay amounts. Similarly, many Electronic Health Record (EHR) systems now use Surescripts' Real-Time Prescription Benefit (RTPB) tool. As of early 2024, 72% of EHR systems had adopted this, allowing doctors to see your specific cost at the point of prescribing. If your doctor's office doesn't seem to have this, politely ask if they can run a real-time benefit check.

Navigating Medicare Part D Changes in 2025 and 2026

If you are on Medicare, the landscape is shifting dramatically thanks to the Inflation Reduction Act. Here is what you need to know for the current year.

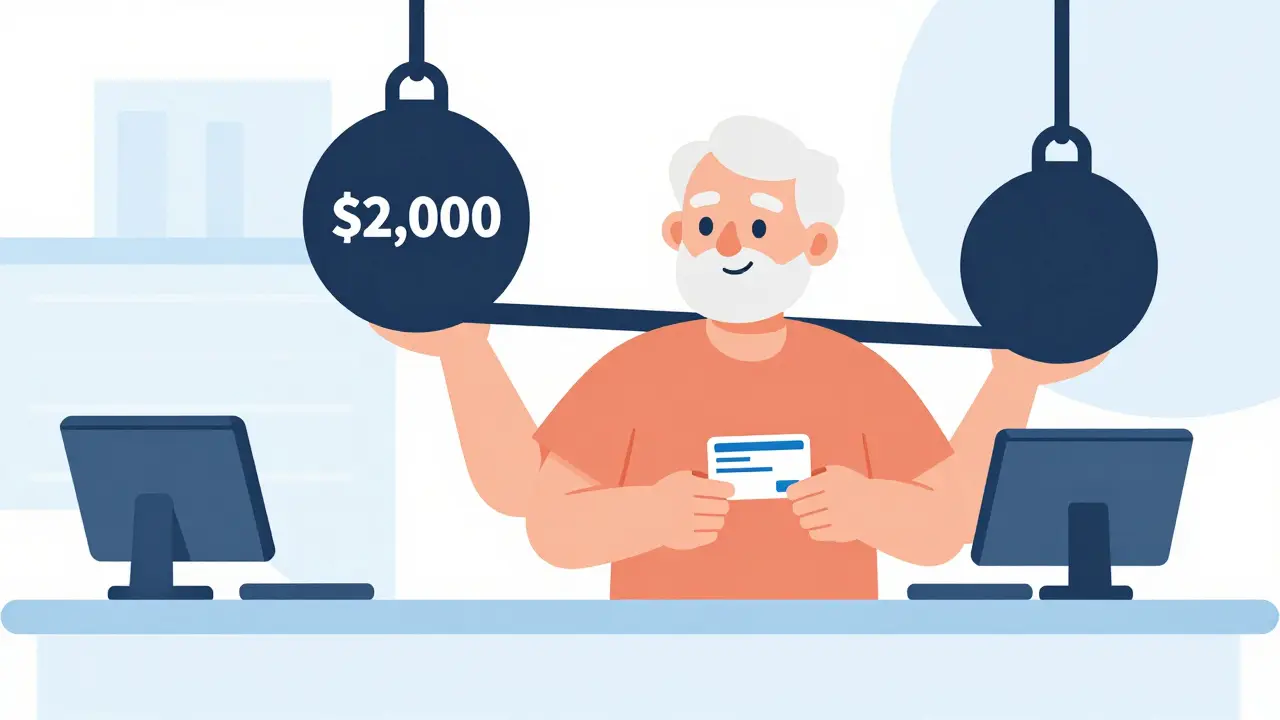

Starting in 2025, Medicare Part D beneficiaries benefit from a hard out-of-pocket maximum of $2,000 annually. This was reduced from $8,000 in 2024. In 2026, this cap remains at $2,000 according to Centers for Medicare & Medicaid Services (CMS) documentation. Once you hit this limit, you pay nothing more for covered drugs for the rest of the year. This is a game-changer for seniors managing chronic conditions.

Additionally, insulin is capped at $35 per month per covered insulin drug. If you are prescribed multiple insulins, you pay $35 for each one. Vaccinations are also free.

A critical new feature is the Medicare Prescription Payment Plan, which allows beneficiaries to spread out high prescription costs over monthly installments rather than paying the full amount at the pharmacy counter. Implemented in 2024 and fully accessible in 2025, this plan helps smooth out cash flow. However, keep in mind that enrolling late in the year (after September) reduces the benefit, as there are fewer months left to spread the payments. CMS recommends reviewing your expected annual drug costs early in the year to decide if this plan makes sense for you.

| Feature | Medicare Part D (2026) | Commercial Insurance (Typical) |

|---|---|---|

| Annual Out-of-Pocket Max | $2,000 (Hard Cap) | Varies; often none for specialty drugs |

| Insulin Cost Cap | $35/month per drug | Depends on plan tier/formulary |

| Payment Plans | Yes (Prescription Payment Plan) | Rarely offered directly by insurers |

| Prior Authorization Rate | High for specialty drugs | Very High (up to 68% for specialty) |

Strategies for When Your Drug Isn't Covered

Sometimes, despite your best efforts, the medication isn't on your formulary. According to the Patient Advocate Foundation, 43% of prescription cost issues stem from medications not being covered. Don't panic. Here is your action plan.

1. Request a Prior Authorization (PA): Your doctor can submit a PA to your insurer, explaining why this specific drug is medically necessary for you. About 68% of cases involving non-covered drugs are resolved this way. It takes time, so start the process immediately.

2. Apply for a Formulary Exception: Similar to a PA, this asks your insurance plan to make an exception to their rules and cover the drug.

3. Look for Manufacturer Assistance: Visit the pharmaceutical company's website. Most major manufacturers have "Patient Assistance Programs" (PAPs) that provide free or low-cost drugs to uninsured or underinsured patients who meet income guidelines.

4. Switch Therapies: Work with your doctor to find a similar drug that is on your preferred tier. Often, there are older, off-patent drugs that are highly effective and much cheaper.

Timing Is Everything: When to Have the Conversation

The optimal time to discuss costs is during the provider visit, before the prescription is written. The AMA's STEPS Forward module emphasizes this timing. Once the prescription is sent electronically to the pharmacy, it becomes harder to change without restarting the process.

If you realize after the fact that the cost is too high, call your insurance company's customer service line. Have your National Drug Code (NDC) number ready-you can find this on your prescription label or online. While average wait times reached nearly 15 minutes in 2023, getting a direct quote from your insurer is the most accurate method. Alternatively, use the Medicare.gov "Plan Finder" tool during the Annual Enrollment Period (October 15-December 7) to compare how different plans handle your specific medications for the upcoming year.

Remember, you are the CEO of your own health. Asking about cost is not just smart budgeting; it's a vital part of ensuring you stay healthy. Don't let embarrassment stop you from having this conversation. Your doctor wants you to take your medication, and they can only do that if you can afford it.

Should I use my insurance or a GoodRx coupon?

It depends on your deductible and the drug's tier. If you haven't met your deductible, a GoodRx coupon might be cheaper than your insurance copay. However, payments made with GoodRx generally do not count toward your annual deductible. If you expect to spend heavily on medications this year, using your insurance is usually better because it progresses you toward your out-of-pocket maximum. Always compare both prices at the pharmacy counter.

What is the Medicare Prescription Payment Plan?

The Medicare Prescription Payment Plan allows Part D beneficiaries to pay for their prescription drugs in monthly installments instead of all at once at the pharmacy. This helps manage cash flow, especially for expensive specialty drugs. The total amount you pay cannot exceed your annual out-of-pocket maximum ($2,000 in 2026). It is optional and must be enrolled in through your Part D plan.

Can my doctor switch my prescription to a cheaper alternative?

Yes, absolutely. Doctors often prescribe based on efficacy and safety, but they may not always know the exact cost to you. If you mention affordability is a concern, they can often switch you to a generic version or a different brand within the same therapeutic class that is covered by your insurance. Never stop taking medication without consulting your doctor first.

What is prior authorization?

Prior authorization (PA) is a process where your insurance company requires your doctor to prove that a specific medication is medically necessary before they will cover it. This is common for expensive specialty drugs or when cheaper alternatives exist. Your doctor's office handles the paperwork, but it can delay your access to the medication by several days.

How do I find out if a drug is on my formulary?

You can log in to your insurance company's member portal and search their formulary list. Alternatively, call the customer service number on the back of your insurance card. Ask specifically for the "tier" of the medication. Tier 1 is usually the cheapest, while higher tiers indicate higher costs. Pharmacists can also check this for you, but doing it beforehand saves time.

rebecca torres

June 14, 2026 AT 14:37honestly the tier system is just corporate speak for how much they want to squeeze you before you break

Brett Webster

June 15, 2026 AT 05:11The distinction between using insurance versus a GoodRx coupon is often misunderstood by patients who assume one is universally better. In reality, if you are early in your plan year and have not met your deductible, the cash price via a discount card can be significantly lower than the full negotiated rate your insurance requires you to pay out of pocket. However, this creates a catch-22 where those savings do not apply toward your annual maximum. It is crucial to calculate your projected annual drug spend against your deductible threshold to determine the most fiscally responsible path forward.

Aditya Singh

June 15, 2026 AT 16:24From an international perspective, the complexity of formulary tiers and prior authorization protocols represents a significant administrative burden that detracts from clinical efficiency. The integration of Real-Time Prescription Benefit tools within Electronic Health Records is a commendable step towards interoperability and cost transparency. We must advocate for systemic reforms that prioritize patient-centric financial literacy and reduce the cognitive load on healthcare providers regarding pharmacoeconomic assessments.

Lee Coates

June 17, 2026 AT 09:25Another day another government program trying to save us from ourselves :P Like we need more bureaucracy to tell us what pills to buy when the real issue is that our local pharmacies are all owned by three giant corporations anyway lol

Erin Livengood

June 18, 2026 AT 16:00I feel like talking about money with doctors is like asking a chef if the soup is too salty while you're already eating it; it feels awkward but necessary for survival. We treat health as this sacred temple where commerce shouldn't exist, yet every single pill is a commodity wrapped in white plastic. It’s a beautiful tragedy really, how we’ve built a system where you have to beg for the very thing keeping your heart beating.

shreya sinha

June 19, 2026 AT 22:54It is profoundly disheartening to observe the sheer negligence inherent in a healthcare framework that necessitates such exhaustive consumer advocacy merely to secure basic medicinal necessities, thereby exposing the fundamental moral bankruptcy of prioritizing profit margins over human well-being and highlighting the urgent need for comprehensive structural reform to ensure equitable access to life-sustaining treatments for all citizens regardless of their socioeconomic status or insurance coverage nuances.

Sherry Wheeler

June 20, 2026 AT 21:37This is absolutely vital information! I cannot stress enough how empowering it feels to finally understand the jargon. When I learned about the Medicare Payment Plan, it felt like finding a secret door in a maze that had been trapping me for years. Your health is your wealth, and knowing these tools is like having a shield against the chaos of modern medicine!

Cecilia McGuinness

June 21, 2026 AT 12:53i was so confused abt the deductible part until i read this thanks for breaking it down simpley its crazy how hard they make it

Miranda River

June 21, 2026 AT 20:00people think reading the fine print helps but really the insurance companies just change the rules every time you blink its like playing chess with someone who keeps moving the board pieces around while you're not looking so why bother trying to understand it at all

Brandon Brodsky

June 23, 2026 AT 00:23Sure, ask your doctor about costs. Because clearly, the reason my blood pressure medication costs $400 is because I didn't ask nicely enough during my 15-minute appointment. Groundbreaking insight here, truly.

Ganesh Honikol

June 23, 2026 AT 13:50It is indeed imperative that patients engage in proactive dialogue with their healthcare providers regarding the financial implications of prescribed therapeutics, as this collaborative approach not only fosters a sense of agency but also ensures adherence to treatment protocols which is paramount for optimal health outcomes and overall quality of life in the long run :)

AnneKatherine Stiekes

June 24, 2026 AT 16:38the generic switch saved me so much last month just ask always ask

Emily Barnhill

June 25, 2026 AT 08:44We must hold our providers accountable for failing to initiate these critical conversations about cost and coverage. It is unacceptable that patients are left to navigate this labyrinthine system alone without adequate support or guidance from those sworn to protect their well-being. Demand better care now.

Daniella Renzon

June 26, 2026 AT 09:48Living abroad makes me appreciate any clarity on this topic. The stress of not knowing if you can afford meds is universal though. Just take a deep breath and ask the questions. You got this.

Talilla Bailey

June 27, 2026 AT 05:34It is imperative that individuals meticulously review their formulary tiers and deductibles prior to initiating any therapeutic regimen. Failure to do so constitutes a dereliction of personal responsibility in managing one's healthcare expenditures. One must exercise due diligence and interrogate the provider regarding all potential financial liabilities associated with the prescribed intervention.